MANAGEMENT OF CATASTROPHE RISKS

Historically, the Insurance Industry has helped economic development and growth through three core mechanisms, namely risk transfer, risk management and capital accumulation.

In the last two decades, rapid industrialization supported by insurance across the globe has resulted in a growing phenomenon of cluster risks featuring massive infrastructure, buildings , booming economies, and a prolific growth of urban centers.

Most of these developments have led to major concentration of risks, which are exposed to Natural Catastrophic occurrences. Economic growth essentially means that there is more stuff in the way of bush fire, earthquake, flood and so on.

No matter where the properties are located, they are exposed to the risk of Natural Catastrophe. Risks located in the highland areas are more exposed to Earthquake damage, while those in the coastal areas are more exposed to severe flooding and storms.

Natural catastrophes are caused by forces of nature. They include such events as floods, storms, droughts, earthquakes, bush fires, and cold weather. Such events lead to high volume of claims and unless adequate risk control, risk funding and organizational catastrophes plans have been put in place in advance, insurance and reinsurance companies may have difficulty in meeting these claims both financially and operationally.

Natural catastrophe related losses are large and unpredictable. When a catastrophe strikes, the extent of physical damage determines the total economical losses, a large share of which is typically uninsured. The insured losses, however, must be shouldered by the global insurance market. The factors translate into greater insured losses where insurance penetration is high. The level of insured losses also depends on catastrophes’ geography and physical type. Earthquakes are geographical events, while meteorological events are rainstorms, hurricanes. Available data indicate that losses due to Earthquakes (geographical) are on the average less insured than those from storms (meteorological events)

The Global occurrence of disasters resulting in significant losses has become more frequent and severe. The upward trend in overall economic losses in recent decades highlights the global economy’s increasing exposure to natural catastrophes. The losses have been compounded by rising wealth, and increased population concentration in exposed areas such as coastal regions and earthquake prone cities.

The trend in loss development can be attributed to weather related events. Volatile weather patterns and activities are increasing around the world and have resulted in major events such as typhoons, floods, tornadoes etc. These have had big impact on business performance across a wide range of industries. This development has led to an un preceded losses for the global Insurance Market.

Insurers are usually able to aggregate losses arising from the same event to recover from reinsurers and so claims managers must ensure that they have systems in place for their teams to monitor these exposures.

The physical destruction caused by the natural catastrophes triggers a series of adverse effects, such as damaged production facilities, shattered transportation infrastructure and business interruption which results in both direct and indirect losses in the form of forgone output. Beyond these Economic costs are enormous human suffering, and a host of long term socioeconomic consequences.

For property and casualty insurers, catastrophes are defined as infrequent events that cause severe loss, injury, or property damage to a large population of exposures. Whereas most property insurance claims are fairly predictable and independent, catastrophe events are infrequent and claims for a given event are correlated.

SUMMARY OF CATASTROPHIC IN 2013 SUMMARY

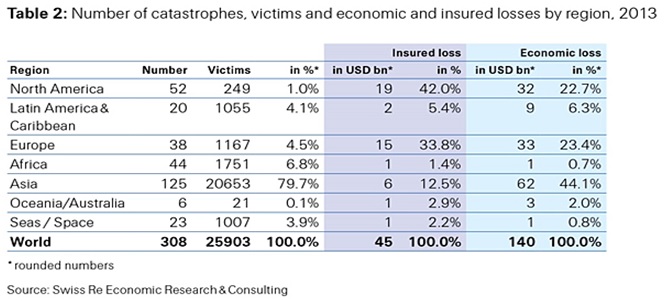

According to the latest sigma study, global insured losses from natural catastrophes and man-made disasters were USD 45 billion in 2013, down from USD 81 billion in 2012. Of the 2013 insured losses, USD 37 billion were generated by natural catastrophes, with hail in Europe and floods in many regions being the main drivers.

Total economic losses from catastrophic events were USD 140 billion, down from USD 196 billion in 2012 and well below the 10-year average of USD 190 billion. The number of victims in disaster events grew to around 26 000 in 2013 from 14 000 the previous year.

Asia was hardest hit by natural catastrophes in terms of economic losses and victims. Typhoon Haiyan in the Philippines in November brought some of the strongest winds ever recorded, alongside heavy rains and storm surges. Around 7 500 people died or went missing, and more than 4 million were left homeless. The second biggest humanitarian disaster of 2013 was the June flooding in the state of Uttarakhand in India, which claimed some 6 000 lives.

Europe suffered the two most expensive natural disaster events in 2013. Massive flooding in central and eastern Europe in May/June after four days of heavy rain caused large-scale damage across Germany, the Czech Republic, Hungary and Poland. Total economic losses were USD 16.5 billion, and the insured loss was USD 4.1 billion. Not long after, in late July parts of Germany and France were hit, this time by severe hailstorms.

The storms struck heavily populated areas in Germany, which, according to latest estimates, generated most of the entire insured loss total of USD 3.8 billion, the largest ever from a hail event, worldwide. Many regions around the world were hit by floods in 2013. The single largest loss-event in North America was extensive flooding in the city of Calgary, Alberta and surrounding area following six days of torrential rain. The economic loss was USD 4.7 billion and the insured loss was USD 1.9 billion. Floods also generated losses in Australia, Asia and South America.

Overall, global insured losses were significantly lower in 2013 than in 2012. This was mainly because of a very quiet hurricane season in the US. Nonetheless, with insurance penetration greater than anywhere else, the US still had the biggest insured loss total last year. This was due to several tornado outbreaks and related thunder and winter

Global protection gap continues to widen

Risk prevention and mitigation measures have progressed in recent years. For instance, the losses from the floods in central and eastern Europe last year would have been much worse had the flood protection measures not been strengthened after the same region suffered severe flooding in 2002. Likewise, a very effective pre-designed evacuation drive saved thousands of lives when Cyclone Phailin made landfall in Odisha, India in October, with winds of up to 260 km per hour.

However, the cyclone destroyed around 100 000 homes and more than 1.3 million hectares of cropland. Kurt Karl, Chief Economist at Swiss Re says: "The total economic loss of Cyclone Phailin is estimated to be USD 4.5 billion, with just a tiny portion covered by insurance. The insurance industry can play a much larger role in helping societies deal with the fallout of disaster events, such as this and Typhoon Haiyan."

The protection gap, the difference between total losses and insured losses, has progressively widened over the last 40 years. Disaster events continue to generate increasing total losses alongside ongoing economic development, population growth and urbanization.

Table 2

MAJOR CATASTROPHIC EVENTS EXPERIENCED UIN THE WORLD

| YEAR | CATASTROPHIC EVENT | COST IN US DOLLARS (Billion) | REMARKS |

| 2011 | Japanese Tsunami | 210 B | |

| 2005 | Hurricane Katrina | 125 B | |

| 1995 | Japanese Earth Quake (Kobe) | 100 B | |

| 2008 | Chinese Earthquake | 85B | |

| 1994 | US Earthquake, North Ridge | 44 B | |

| 2011 | Thai Floods | 40 B | |

| 2008 | Hurricane Ike-US & The Caribbean | 38.3 B | |

| 1998 | China Floods | 30.7 B | |

| 2010 | Chile Earthquake | 30B | |

| 2004 | Japanese Earthquake | 28B |

RISK TRANSFER PROCESS

The risk usually cascade from the policy holders via primary insurers to reinsurance companies. Reinsurers cope with peak risks through diversification, prefunding and risk-sharing with other financial institutions, spread all over the world.

This global risk transfer creates linkages within the insurance Industry (Insurers, Reinsurers and Retrocessionaires) and between insurers and financial markets. Despite the risk transfer being in place, insurers remain fully liable to the policy holder based on the initial contractual obligation, regardless of whether or not the next in line pays up on the ceded risk. Claims for reimbursements will affect the primary insurers, who will only absorb some of the losses, having ceded a share of their exposures to reinsurance companies.

The most important feature of this transaction is the prefunding of insured risks. Premiums are paid in advance for protection against an event that may or may not materialize over the course of the contract. These payments by policy holders generate a steady flow of cash to insurers and reinsurers. Only if and when an event with specified characteristics occurs are claims payments triggered. At all other times, the premium flows are accumulated in the form of assets held against technical reserves.

Losses from insured property first affect the primary insurers, who in turn rely on reinsurers to absorb peak risks. Reinsurers in turn, use their balance sheets and retrocession and securitization arrangements to manage the peak risks.

The volume of insured losses differs substantially across continents, depending on the availability of and demand for insurance. The insurance density will indicate the stage of the region’s economic development. Residents of North America, Oceania and Europe spend significant amounts on insurance, whereas many populous countries in Latin America, Asia and Africa host underdeveloped insurance markets. Poor countries typically lack the financial and technical capacity to provide affordable insurance coverage.

Catastrophe exposures place special demands on insurer’s capitalization and require a distinct risk management approach. Catastrophes represent significant financial hazards to an insurer, including the risk of insolvency, an immediate reduction in earnings and surplus, the possibility of forced asset liquidation to meet cash needs, and the risk of a ratings downgrade. The risk management process for an insurer therefore must integrate all risk management strategies and not just for a single risk, such as catastrophe.

Careful analysis of risks should be carried out at the time of underwriting in order to avoid the error of having massive exposure in the event of occurrence of a Natural Catastrophes as is the current situation, particularly in our region.

BEST PRACTICE FOR CATASTROPHE EXPOSURE MANAGEMENT

Natural catastrophes such as earthquakes, hurricanes, tornadoes, wildfires, and winter storms can jeopardize the financial well-being of an otherwise stable, profitable company.

Catastrophe modeling (also known as cat modeling) is the process of using computer-assisted calculations to estimate the losses that could be sustained due to a catastrophic event. Cat modeling is especially applicable to analyzing risks in the insurance industry and is at the confluence of actuarial science, engineering, meteorology, and seismology.

Catastrophe models are tools that help risk managers effectively assess catastrophe risk and make informed risk management decisions. The Models determine the potential loss to a client’s exposure from natural perils.

They help companies to monitor their aggregate exposures to catastrophes. This is necessary to assess their solvency.

Although these models are in place, they are not robust enough to adequately account for potential losses. In as much as they may not always be right, they never the less provide a catalogue of plausible events, and so can provide loss statistics with reasonable confidence.

While assessing a natural disaster risk quantitatively in a forward looking manner is still relatively a young science and comes with some uncertainties. A lot of leveraging is put historical data, which may be misleading despite the use of sophisticated models in the quest to improve accuracy.

By simulating various combinations of events that may occur in any one period, and the effect these have on risks underwritten by the company, the insurer can plot the annual probability of exceeding a range of loss levels, then take appropriate action, which may include purchasing reinsurance cover and/or reducing its territorial exposure to certain classes.

By incorporating the results of catastrophe models, the following best practices can enable risk managers to take greater control of the risk transfer process and make the best and most cost-effective decisions for their enterprises, bearing in mind that all risk management solutions essentially improve a company's geographic spread of risk, or the time horizon in which to manage its risk – the two most critical elements to consider in a Cat exposure management strategy.

Catastrophe modeling is the best way to identify the extreme events that can threaten an enterprise and to quantify the insurance coverage needed to protect the organization from the financial impacts. Catastrophe models simulate thousands of years of earthquakes, hurricanes, severe thunderstorms, wildfires, winter storms, terrorist acts, and other natural and man-made events. The simulated events are then superimposed over property exposures to determine the likelihood of one or more of events causing a loss. The output of the models provides the full range of potential losses, which an organization can then analyze.

Fortunately, natural and man-made events capable of derailing a company’s operations are rare. However, risk managers must understand the likelihood of these low-frequency, high-impact occurrences so that they can determine how much coverage to buy, what deductible level to choose, and at what cost.

The primary benefit of catastrophe modeling is that it provides a statistical measure of potential losses, so risk managers can align their insurance coverage more closely with their organization’s risk tolerance level. Additionally, by avoiding unnecessary coverage and customizing their corporate risk management program to reflect the realistic probabilities of loss from specific perils, risk managers can allocate risk transfer funds more effectively.

Models also enable side-by-side comparisons of various scenarios — such as the probable cost of certain risk transfer/retention strategies — that can help risk managers and their brokers decide the amount of the deductible as well as the optimal way to apply it. Risk managers can more confidently determine whether the deductible should be a percentage of site replacement cost, a percentage of the aggregate loss, or a fixed sum and whether it should be applied per occurrence (single event) or capped annually.

The acceptance and use of catastrophe modeling within the insurance industry is widespread today and nearly universal for large organizations. Thus, underwriters’ recognition of the technology works in favor of the insurance buyers who include model results with their submissions. Sharing model results with underwriters — particularly results that include a level of detail the underwriter doesn’t normally see — can be a powerful and persuasive negotiating tool during renewal time.

Catastrophe models can improve the quality of the information on which critical business decisions are based, such as:

Marginal impact of acquisition or sale —

when dealing with a large portfolio of properties or multiple-location policies, the risk manager should be aware of how the sale or acquisition of a property may affect the organization’s risk profile. The location, value, and construction type of the properties in question, and their relation to the existing portfolio, can significantly alter the organization’s overall exposure. A catastrophe loss analysis is the best method to determine if a renegotiation is warranted and to quantify the appropriate rebate or preferred additional coverage.

Geographical consolidation or dispersion of operations —

Catastrophe modeling can provide insight into more effective ways of managing exposure to catastrophe risk. Model results provide a clear picture of a company’s geographical distribution of exposures and the key drivers of a company’s catastrophe risk, including which perils, regions, and businesses have the greatest marginal impact on losses. Such information can help businesses fine-tune growth strategies to manage future catastrophe loss potential. The analyses can help determine where business can be expanded without increasing loss potential, as well as areas in which a company is already overexposed to catastrophe losses.

Allocation of insurance costs among business units —

In addition to identifying the contribution of each location to an enterprise’s overall catastrophe risk, a model-based analysis can be used to allocate the cost of insurance back to individual locations or business units. This type of analysis allows organizations to assess fully the net benefit of geographically diverse operations or assets.

In summary, Catastrophe modeling offers enormous value to risk managers — value that continues to increase as the technology evolves and as property values increase in catastrophe-prone areas. Catastrophe modeling enables proactive decision making and strategic planning. As modeling analyses become more accessible — whether in-house, as a service through brokers, or directly from modelers — risk managers are embracing the technology to further their companies’ competitive advantage and make scientifically sound decisions about catastrophe risk management.

Catastrophe Mitigation Strategies

The goal of mitigation is to lessen the financial impact, i.e., reduce loss payments resulting from catastrophes. Three ways to address exposure management via mitigation are:

Modifying the risk

Use premium credits to encourage the use of storm shutters, roof tie-downs, pipe insulation, etc.

Restriction of coverage

Introduce catastrophe peril deductibles; restrictions in policy form; limitations on replacement cost coverage.

Minimize loss adjustment expenses

Effectively administer claims including the creation of a catastrophe claims team and a game plan before an event occurs. Stockpiling of basic resources such as plywood, tarps, etc., as well as plans for their distribution after an event occurs can also significantly reduce the financial impact of catastrophe losses.

Companies can manage their catastrophe exposure, and ultimately their financial position, through various strategies. Broadly speaking, these strategies can be grouped into one of four categories: Avoidance, Mitigation, Retention and Transfer.

Catastrophe Avoidance Strategies

Since it is rarely possible to separate catastrophe risk from other property insurance risk, companies need to selectively manage exposures to minimize the potential for an accumulation of a large number of losses in a single event, i.e. minimize the Probable Maximum Loss (PML) potential. This involves selectively canceling or non-renewing policies in areas of peak exposure.

In order to selectively manage a portfolio to minimize the PML potential, companies need the ability to quantify and identify peak exposure areas. Sophisticated computer models are readily available to help companies understand and manage their portfolios, to achieve a balance between the need to bear risk, and the need to preserve the financial integrity of their companies in the face of catastrophe exposures.

The industry needs to pursue a blend of internal and external solutions to ensure two key factors:

- Ability to identify, quantify and estimate the chances of an event occurring and the extent of losses, likely and

- The ability to set adequate risk premiums.- Once companies have an understanding of their catastrophe potential, they can effectively formulate underwriting guidelines to act as control valves on their catastrophe loss potential. Underwriting guidelines can be used to decrease writings in overly exposed areas, as well as encourage new business opportunities in under exposed regions.

Catastrophe Retention Strategies

A retention strategy focuses on a company's ability to bear catastrophe losses within the framework of its own financial position. One tactic in the face of severe loss potential is to strengthen the capital position of the company. This can be accomplished pre-event or post-event through a variety of capital-raising methods. Given the extremely volatile impact of catastrophe losses on a company's financial position, it is important that a company's constituents, including policyholders, shareholders, and regulators, fully understand the associated risks of this strategy, in particular if it is used aggressively.

Pre-event planning allows a company to negotiate from a position of strength. After an event, a company's financial position could be impaired, significantly increasing the cost of new capital. An alternative is to arrange contingent financing, i.e., post-event capital that is arranged before the event occurs.

Catastrophe Transfer Strategies

A transfer strategy shifts the potential financial impact of catastrophe events to other parties, typically for a predetermined fee. This fee reflects the long-term expected cost of losses being shifted, as well as a margin to cover expenses and the cost of capital used to absorb the potential catastrophe volatility. This strategy shifts risk to those better able to absorb catastrophe losses due to either stronger financial resources or a more diversified property portfolio.

It is therefore important to understand the Potential Magnitude and Frequency of Large Losses

Knowing how big potential catastrophes can be and how often they are likely to occur will help risk managers avoid either overbuying or under buying insurance. Many companies insure to the probable maximum loss (PML), but a PML does not provide information about the probability that an event will occur. A better way to manage catastrophe risk is to understand the likelihood of various levels of potential losses and insure against those probabilities. In addition, knowing where the large losses (and business interruptions) are most likely to occur is useful for disaster recovery and operations planning.

EXPOSURE TO CATASTROPHES AT MACRO INSURANCE LEVEL

In most countries of Africa, Insurance penetration is very low, and is estimated at a mere 2%. This implies that the majority are not insured. This simply means that there is a considerable insurance protection gap with regard to Natural Catastrophe protection, and as a result, economic losses are not getting financed as required.

The uninsured mass at the bottom of the population pyramid are usually adversely affected by the occurrences of the Natural Perils. Not only do they suffer economically on account of loss to their property and livelihood, they also face personal crisis due to hospitalization and death. To cover the bottom of the population pyramid, from such unfortunate events, the Regional Government has always come out with handouts whenever disasters occur. This may not be satisfactory as the hand outs are usually politically motivated.

The best way to assist this uninsured population is to create catastrophe programme that are well structured to assist the affected. Whilst Governments could offer monetary aid to victims of such events, this aid to victims can be augmented though such a catastrophe programme.

The Insurance Industry has played significant role in mitigating losses caused by the occurrence of these Natural Perils. Unfortunately, the Whole of the Insurance Industry has failed to communicate effectively to the society at large the important role it plays in managing the risks that individuals and societies face in their day-to-day lives. Lack of this information could be one of the causes of low penetration as mentioned above.

Interestingly, according to Lloyds global Report, a 1% rise in insurance penetration translates into a 13% reduction in uninsured losses, 22% reduction in taxpayer’s contribution following disaster and a 2% rise in GDP in investment funds. Hence any increase in insurance penetration would benefit all stakeholders.

KENNETH O OBALLA

TRAINING MANAGER.

ZEP-RE (PTA-REINSURANCE COMPANY)